What if your W-2 didn’t matter when you applied for a rental loan?

DSCR loans underwrite the property, not your paycheck.

That flips the checklist.

Lenders care about cash flow, reserves, credit quality, and down payment size.

Read on for the numbers that matter: typical DSCR thresholds (about 1.0 to 1.25 and up), the credit-score bands lenders use, and down-payment ranges by property type.

You’ll also get a quick screen to spot deals that pass or fail before you waste time.

Short, practical, and focused on tradeoffs.

Core DSCR Loan Requirements Investors Must Meet

DSCR loan requirements focus on property cash flow, not W-2s or tax returns. Most lenders want minimum debt service coverage ratios between 1.0 and 1.25. That means your property needs to generate at least as much net operating income as the annual mortgage payment, and usually 15% to 25% more. Credit score minimums typically sit between 620 and 660, but best pricing and higher loan-to-value options usually need a score of 700 or better. Down payment expectations shift with property type. Single-family rentals often need 20% to 25% down, while 2 to 4 unit buildings, condos, or short-term rentals commonly ask for 25% to 40%.

Loan-to-value ratios reflect how much risk a lender will swallow and how strong you look as a borrower. Conservative lenders cap LTV at 70%. More flexible programs stretch to 75% or 80% if the deal’s solid and your DSCR and credit look good. Reserve requirements bounce around—expect anywhere from 3 to 12 months of principal, interest, taxes, insurance, and association dues (PITIA) sitting in liquid assets at closing, with most investor targets landing between 6 and 9 months. Lenders also dig into property types. Residential 1 to 4 unit rentals qualify easiest, while properties with occupancy problems, title clouds, or uninsurable conditions get rejected fast.

The six primary investor requirements are:

- DSCR minimums: 1.0 to 1.25 depending on lender, stronger programs prefer 1.15 or higher

- Credit score ranges: 620 to 660 floor, 700+ for optimal pricing and higher LTV

- Down payment percentage: 20 to 25% for single-family, 25 to 40% for multi-unit or specialty properties

- Reserve expectations: 3 to 12 months PITIA, typical requirement 6 to 9 months

- Eligible property types: 1 to 4 unit residential rentals, condos with approval, some short-term rentals with documentation

- Key disqualifiers: DSCR below lender minimum, inadequate reserves, unverifiable rent, poor property condition, recent bankruptcy or foreclosure

DSCR Metrics and How Lenders Evaluate Cash Flow

DSCR (debt service coverage ratio) measures how many dollars of net operating income a property produces for every dollar owed in annual debt service. The formula is straightforward: DSCR = Net Operating Income ÷ Annual Debt Service. Net operating income equals gross rental income minus operating expenses like property taxes, insurance, repairs, management fees, and HOA dues. Annual debt service is the sum of all twelve monthly mortgage payments, including principal and interest. If a property generates $24,000 in NOI and the annual mortgage payment totals $20,000, the DSCR is 1.20. That’s $1.20 of income for every $1.00 of debt.

Lenders read DSCR levels as risk signals. A DSCR below 1.0 means the property loses money every month and can’t cover its own payment. A DSCR of exactly 1.0 breaks even, leaving no cushion for vacancies, surprise repairs, or market downturns. Most lenders consider 1.15 to 1.20 the comfort zone, providing enough margin to absorb typical landlord expenses without defaulting. DSCR above 1.25 opens the door to better pricing, higher leverage, and faster approvals. The cash flow buffer gives lenders confidence the loan will perform even if rents dip or costs rise.

| DSCR Level | Meaning | Typical Lender Response |

|---|---|---|

| Below 1.0 | Property income does not cover debt service (negative cash flow) | Decline or require large compensating factors (high equity, strong reserves, excellent credit) |

| 1.0 | Break-even; income exactly equals debt service | Some lenders approve with stricter terms; others decline or require rate/LTV adjustments |

| 1.15–1.20 | 15–20% cushion above debt service | Standard approval zone; competitive pricing and moderate reserve requirements |

| 1.25+ | Strong positive cash flow; 25%+ margin | Best pricing, higher LTV options, reduced reserve requirements, faster underwriting |

Many lenders stress-test the debt service side of the equation by calculating DSCR using a qualifying interest rate instead of the actual note rate. If your loan closes at 6.5% but the lender underwrites at 7.5%, your monthly payment (and required DSCR) goes up, forcing you to show more income cushion even though your real payment is lower.

Property Types Eligible Under DSCR Loan Requirements

Single-family rental homes form the core of DSCR lending. These properties (detached houses, townhomes, and similar 1-unit structures) qualify most easily because rental demand is broad, resale markets are liquid, and appraisers find strong comparable data. Lenders treat them as lower-risk collateral and often extend the best pricing and highest LTV ratios to single-family deals with verified leases and stable neighborhoods.

Two-to-four-unit multifamily properties also qualify under most DSCR programs, though underwriting becomes more cautious as unit count rises. Duplexes, triplexes, and fourplexes generate higher gross rents but also carry higher operating expenses, vacancy risk, and maintenance costs. Lenders typically require larger down payments (25% to 30%) and stricter DSCR minimums for these buildings. Condos and planned unit developments (PUDs) are eligible if the project meets lender condo-approval standards, which screen for financial health of the HOA, owner-occupancy ratios, and completion status. Non-warrantable condos (projects that don’t meet Fannie or Freddie guidelines) can still qualify for DSCR loans but often face tighter LTV caps and higher rates.

Eligible property tiers include:

- Single-family rentals (SFRs): broadest approval, best pricing, LTV up to 80% with strong DSCR and credit

- 2 to 4 unit multifamily: common approval with 25 to 30% down, stricter DSCR thresholds

- Condos and PUDs: require project approval; warrantable condos preferred, non-warrantable accepted at tighter terms

- Short-term rentals (STRs): permitted by some lenders with documented rent history, permits, market rent analysis, and often higher reserves; expect closer expense scrutiny

Every DSCR loan requires a full appraisal with a Form 1007 rent schedule, which estimates the property’s market rent based on comparable rentals in the area. Lenders use the lesser of actual rents (if leased) or appraised market rents to calculate NOI, so inflated lease agreements or unsupported rental claims get caught during underwriting.

DSCR Loan Documentation Requirements for Investors

DSCR loans simplify personal income verification but tighten property documentation. You won’t submit W-2s, pay stubs, or tax returns in most cases, but lenders will demand proof the property can service the debt. Start with the appraisal and Form 1007 rent schedule. Lenders order the appraisal, and the rent schedule becomes the foundation of your DSCR calculation. If the property is already leased, submit executed lease agreements or a rent roll showing tenant names, lease terms, monthly rent, and security deposits. New purchases without existing tenants rely entirely on the appraiser’s market rent estimate.

Bank statements verify reserves and down payment funds. Lenders typically ask for the most recent two months of statements from all accounts you’ll use to close, and they’ll trace large deposits to confirm the money is yours and not borrowed. If you’re buying through an LLC or corporation, include formation documents (articles of organization, operating agreement, and any amendments) plus an EIN letter from the IRS. Personal identification (driver’s license or passport) and a signed credit authorization round out the borrower-side paperwork.

Required documentation includes:

- Appraisal with Form 1007 rent schedule (ordered by lender)

- Executed lease agreements or rent roll (if property is leased)

- Bank statements (typically last 2 months, all accounts used for reserves and down payment)

- LLC/corporation formation documents and EIN letter (if applicable)

- Insurance quotes or binder showing hazard coverage and flood if required

- Property tax bill or tax estimate from county assessor

- Purchase contract and any addenda (for purchases)

- Title commitment and preliminary title report

- Operating statements or profit-and-loss for the property (if available)

- STR permits, business licenses, or platform income history (for short-term rentals)

Lender-specific variations show up most often around short-term rental documentation. If you’re financing an Airbnb or vacation rental, expect to provide platform income reports (12 months preferred), local permits or occupancy licenses, and market studies supporting your projected rental income. Some lenders apply haircuts to gross STR income, reducing it by 20% to 40% to account for cleaning, platform fees, vacancy, and seasonality, which lowers your calculated NOI and DSCR.

How Borrower Financial Strength Influences DSCR Loan Terms

Credit score tiers directly affect interest rate pricing and LTV flexibility. A borrower with a 750 FICO might receive a rate 0.5% to 1.0% lower than a borrower at 660, even if both properties show identical DSCR. Lenders use credit-based pricing adjustments that stack on top of base rates, so stronger credit unlocks not just approval but also better monthly cash flow and lower lifetime interest costs. Higher credit also expands what you can borrow. Lenders willing to go to 80% LTV at 720+ often cap at 70% or 75% for scores below 680.

Reserve strength sends a secondary confidence signal. When a borrower holds 12 months of PITIA in liquid reserves instead of the minimum 6 months, underwriters see a buffer against vacancy, repairs, and income disruption. That comfort translates into fewer pricing hits, faster approval timelines, and willingness to approve borderline DSCR deals or properties with slightly elevated risk profiles. Reserves also matter when scaling. Investors managing five or ten properties face higher aggregate risk, and lenders protect themselves by requiring deeper cash cushions per door.

Putting more down creates pricing tiers and opens up loan structure flexibility. Borrowers willing to put 30% down instead of 20% often unlock better base rates, access to interest-only periods, and fewer prepayment penalty constraints because lower LTV reduces lender loss exposure if the property underperforms or markets soften. High-leverage deals (75% to 80% LTV) require compensating strength elsewhere, typically a DSCR above 1.20, credit above 700, and reserves exceeding baseline requirements. If any one piece weakens, lenders either decline or offset the risk with rate adjustments and tighter terms.

DSCR Underwriting Differences: How Lenders Calculate NOI and Predict Debt Service

Underwriters rarely accept gross rent as net operating income. They apply adjustments to reflect real-world operating conditions and protect against borrower optimism. Vacancy assumptions are standard. Most lenders reduce gross rent by 5% to 10% to account for turnover, even if the property is currently leased, because no rental stays occupied 365 days a year forever. Management fees get deducted next, typically 8% to 10% of gross rent, whether you self-manage or hire a property manager, because lenders assume professional management cost when underwriting long-term risk. Insurance and property tax figures come from actual quotes and county records, not borrower estimates, and lenders often add a buffer if taxes are appealing or insurance markets are hardening.

Common NOI adjustments include:

- Vacancy allowance: 5 to 10% of gross rent

- Property management fee: 8 to 10% of gross rent

- Property tax: actual bill or assessed value estimate

- Hazard and flood insurance: actual quote or lender-required minimum

- HOA or association dues: actual monthly fee

| Payment Type | Used For | Impact on DSCR |

|---|---|---|

| Actual Payment (note rate, full amortization) | Monthly cash flow and investor planning | DSCR calculated on real debt service; may understate lender risk if rates rise |

| Qualifying Rate Payment (stress-tested rate, full amortization) | Underwriting cushion; protects lender if rates adjust or refi is needed | DSCR reduced by higher payment assumption; forces stronger NOI to qualify |

| Interest-Only Payment (interest only for 5–10 years, then amortization) | Cash flow optimization during hold period | DSCR calculated on IO payment or post-IO amortized payment depending on program; may require 1.25+ DSCR on fully amortized payment |

Debt service calculations also vary by loan structure. Fixed-rate loans use straightforward principal-and-interest payments over the full amortization term, but adjustable-rate and interest-only loans introduce complexity. Some lenders calculate DSCR using the initial interest-only payment, which inflates the ratio and makes qualification easier, while others underwrite to the fully amortized payment that kicks in after the IO period ends, forcing borrowers to show enough income to handle the higher future payment. ARMs may be stress-tested at the first adjustment cap or a margin above the index, not the introductory teaser rate.

DSCR Interest Rates, Terms, and Loan Structures

DSCR loan interest rates typically range from 5.0% to 9.0%, depending on credit score, down payment, property type, DSCR strength, and lender channel. Expect rates roughly 0.5% to 2.0% higher than conventional conforming mortgages because DSCR loans are non-QM or portfolio products without government backing or secondary-market liquidity. Borrowers with credit above 720, DSCR above 1.25, and 25% down payments land near the lower end of the range, while deals with marginal DSCR, weaker credit, or higher leverage push toward the upper end.

Loan terms mirror investor hold strategies. Thirty-year fixed-rate amortization is the most common structure, offering predictable payments and long-term cash flow stability for buy-and-hold investors. Adjustable-rate mortgages (ARMs) come in 5/6, 7/6, and 10/6 configurations (fixed for the initial period, then adjusting every six months based on an index plus margin). ARMs start with lower rates than fixed loans, making them attractive for investors planning to sell or refinance within five to seven years, but they carry rate-increase risk if the hold period extends. Interest-only structures allow investors to pay only interest for the first 5 to 10 years, maximizing monthly cash flow and freeing capital for additional acquisitions, then switch to fully amortized payments. Lenders typically charge 0.25% to 0.50% higher rates for IO options and may underwrite DSCR using the post-IO payment to ensure borrowers can handle the jump.

Common loan structures include:

- 30-year fixed-rate: predictable payment, highest initial rate, best for long holds

- 5/6, 7/6, 10/6 ARMs: lower initial rate, adjusts after fixed period, suitable for medium-term holds or planned refinances

- Interest-only (5 to 10 year IO period): lowest initial payment, maximizes cash flow, requires strong DSCR on amortized payment for approval

- 40-year amortization (sometimes with IO): extended term lowers payment, increases total interest, less common but available from portfolio lenders

Prepayment penalties are standard on DSCR loans and protect lenders from early payoff that cuts interest income. Typical structures include step-down schedules like 3-2-1 (3% penalty in year one, 2% in year two, 1% in year three, then none) or 5-4-3-2-1 for longer lockouts. Penalties apply to the outstanding principal balance at payoff, so selling or refinancing a $400,000 loan in year two of a 3-2-1 penalty costs $8,000. Some programs offer reduced or no prepayment penalties in exchange for slightly higher interest rates or lower LTV, giving investors flexibility to exit early if market conditions or personal plans change.

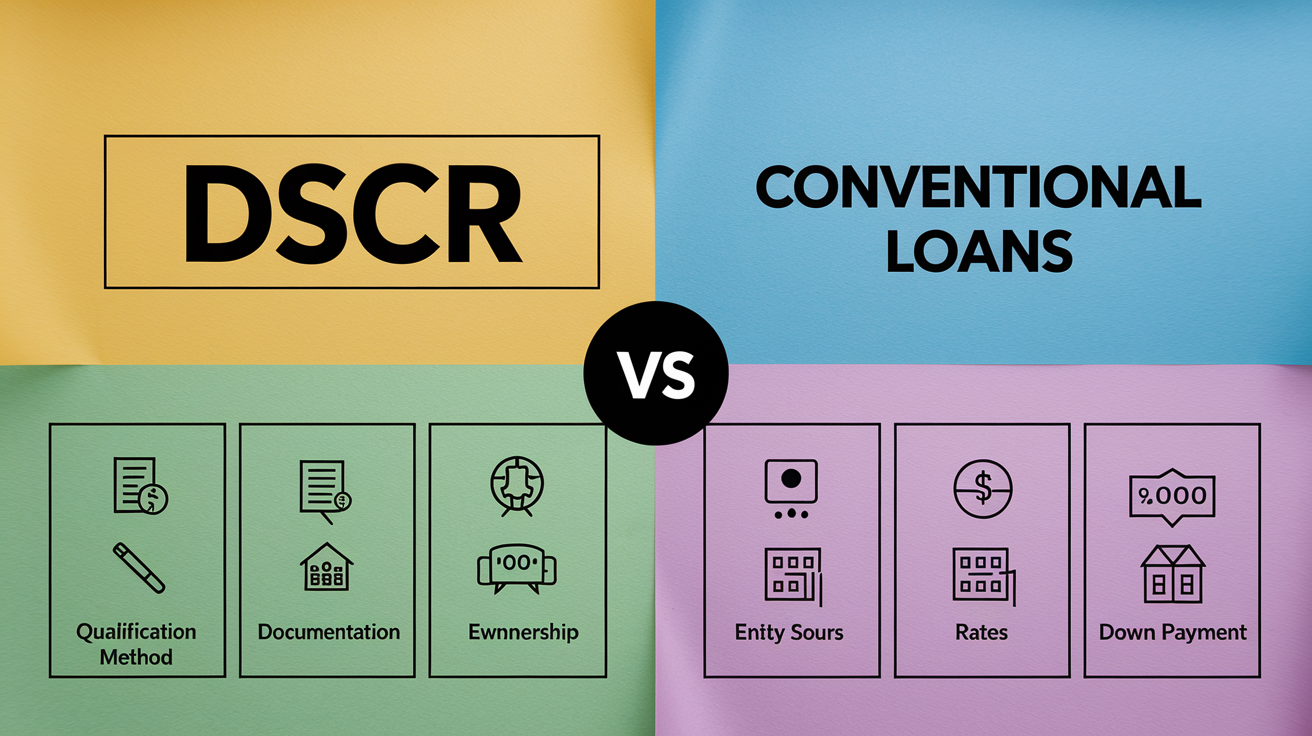

How DSCR Loans Compare to Conventional Investment Mortgages

DSCR loans and conventional investment mortgages both finance rental properties, but they follow opposite underwriting logic. DSCR programs qualify borrowers on property cash flow (net operating income must cover debt service) without requiring W-2s, tax returns, or personal income verification. Conventional loans, by contrast, use debt-to-income ratio (DTI) calculations that compare the borrower’s total monthly debts (including the new mortgage) to their documented gross income from employment, self-employment, or other sources. That difference makes DSCR loans ideal for self-employed investors, retirees, or anyone with income that’s hard to document, while conventional loans favor W-2 wage earners with clean tax returns and low existing debt.

Ownership structure rules diverge sharply. DSCR lenders routinely approve loans to LLCs, corporations, and partnerships, letting investors separate personal liability from rental assets and scale portfolios without personal name clutter. Conventional conforming loans (Fannie Mae, Freddie Mac) require individual borrowers and restrict the number of financed properties (typically four to ten mortgages maximum), forcing portfolio investors to switch to commercial or DSCR products once they hit the ceiling.

| Feature | DSCR Loans | Conventional Loans |

|---|---|---|

| Qualification method | Property cash flow (DSCR = NOI ÷ debt service) | Borrower income and DTI (total debts ÷ gross income) |

| Documentation | Lease, rent roll, appraisal, reserves; no tax returns or pay stubs in most programs | W-2s, tax returns, pay stubs, employment verification, asset statements |

| Entity ownership | LLC, corporation, partnership allowed and common | Individual borrowers only (no entities on conforming loans) |

| Interest rates | Typically 0.5–2.0% higher than conventional | Lower rates due to agency backing and secondary market liquidity |

| Down payment | 20–40% depending on property type, credit, DSCR | 15–25% for investment properties (higher than owner-occupied) |

The tradeoff is cost. DSCR loans carry higher interest rates (often 0.5% to 2.0% above conventional) and require larger down payments and reserve cushions because lenders price in the credit and documentation risk they’re not capturing through income verification. Conventional loans offer better pricing and lower equity requirements but demand tax-return transparency and personal income proof that many real estate investors either can’t or don’t want to provide.

Improving DSCR to Meet Investor Loan Requirements

If your property’s DSCR falls short of lender minimums, five levers can push the ratio higher. Raising rents is the most direct path. Every $100 per month in additional rent adds $1,200 to annual NOI, which flows straight into the DSCR numerator. Check rent comps carefully. If comparable properties are leasing for 10% more than your current lease, a renewal or tenant turnover gives you a clean opportunity to adjust. Reducing operating expenses attacks the NOI equation from the cost side. Shopping insurance annually, appealing property tax assessments, and negotiating lower management fees or handling more tasks yourself all increase the income available to cover debt service.

Refinancing to a lower interest rate or longer amortization term reduces your monthly debt service, which lowers the annual debt service denominator and improves DSCR even if NOI stays flat. If rates have dropped since your original loan or your credit has improved, a rate-and-term refinance can turn a 1.10 DSCR into a 1.20 without touching the property. Interest-only loan structures go further. Eliminating principal payments for the IO period cuts monthly payments significantly, inflating DSCR during the interest-only years, though lenders may still underwrite to the fully amortized payment.

Six strategies to improve DSCR:

- Increase rent to market rate using recent comparable leases

- Reduce operating expenses by shopping insurance, appealing taxes, or self-managing

- Refinance to a lower interest rate or longer amortization to reduce monthly debt service

- Switch to an interest-only loan structure (if lender underwrites on IO payment)

- Make a larger down payment to reduce loan amount and lower debt service

- Improve rent documentation accuracy. Use signed leases, not estimates, and provide 12-month payment history to eliminate lender haircuts

Documentation accuracy also moves the needle. Lenders apply conservative assumptions when rent proof is weak (using lower market rents, applying large vacancy reserves, or discounting projected income). Clean, verified leases with 12-month payment histories and tenant contact information give underwriters confidence to use actual rents instead of discounted estimates, which can swing DSCR by 0.05 to 0.15 points on borderline deals.

DSCR Loan Application Workflow and Common Approval Pitfalls

The DSCR loan process starts with prequalification, where you share basic property details (address, purchase price or current value, estimated rent, property taxes, and insurance) and lenders calculate a preliminary DSCR using those inputs plus your credit score and down payment amount. If the initial DSCR clears the lender’s minimum and your credit and equity meet program guidelines, you move into full application. Submit the documentation checklist (signed purchase contract, bank statements, entity formation docs, insurance quotes) and the lender orders the appraisal with the critical Form 1007 rent schedule.

Underwriting begins once the appraisal arrives. The underwriter recalculates DSCR using the appraised market rent (or actual lease rents, whichever is lower), applies standard expense assumptions and vacancy reserves, and confirms your debt service figure using the proposed loan amount, interest rate, and term. They verify reserves, review credit for recent delinquencies or derogatory marks, and check title and insurance for liens, easements, or coverage gaps. If everything aligns, you receive conditional approval with a list of conditions to clear (updated insurance binder, proof of reserve seasoning, signed lease if tenant-occupied, or repairs identified in the appraisal).

Turnaround times are typically faster than conventional loans because there’s no employment verification, no tax-return analysis, and no mortgage credit certificate or gift-letter complexity. Many DSCR lenders close in 15 to 25 days from application to funding, especially on refinances or cash purchases where appraisal is the only third-party delay. The streamlined doc list and property-first focus let underwriters move quickly when the numbers work and the file is clean.

Seven common approval pitfalls include:

- Insufficient reserves: borrower shows only 3 months PITIA when lender requires 6 or more

- Unverifiable rent: no signed lease, rent estimate unsupported by comps, or tenant contact information missing

- DSCR below threshold: actual or appraised rent too low, or expenses higher than borrower projected

- Property condition issues: deferred maintenance, code violations, or appraisal safety concerns requiring repairs before closing

- Title or insurance problems: unresolved liens, easement disputes, or inability to obtain hazard/flood coverage

- Large unexplained deposits: recent bank account activity lender can’t source, triggering suspicion of borrowed down payment funds

- Recent credit events: new collections, charge-offs, late payments, or bankruptcies inside lender seasoning windows (commonly 2 to 7 years)

Final Words

In the action we listed the exact criteria lenders look for: DSCR minimums, credit ranges, LTV and down payment norms, reserve expectations, eligible property types, and common disqualifiers.

We showed how DSCR is calculated from NOI and debt service, how underwriting adjusts the numbers, what docs lenders expect, and which loan structures and pitfalls to watch.

Next steps: run a quick DSCR calc, confirm credit and reserves, assemble rent rolls and appraisal docs, then shop lenders.

Use DSCR loan requirements for investors as a practical checklist while you move forward. You’ll make steadier choices.

FAQ

Q: What core DSCR loan requirements must investors meet?

A: The core DSCR loan requirements for investors are a property DSCR generally 1.0–1.25+, credit scores commonly 620–700+, down payments 20–40% by property type, LTV around 65–80%, and reserves of 3–12 months PITIA.

Q: How is DSCR calculated for investment property loans?

A: The DSCR is calculated as NOI divided by annual debt service (NOI = rent minus operating expenses). A DSCR under 1.0 shows a shortfall; 1.15–1.25+ is what many lenders prefer.

Q: Which property types are eligible for DSCR loans?

A: The property types eligible for DSCR loans include single‑family rentals, 2–4 unit multifamily, condos/PUDs, and some short‑term rentals with documented rents; 5+ unit buildings are usually treated as commercial.

Q: What documentation is required for a DSCR loan application?

A: The DSCR loan documentation required includes leases or a rent roll, bank statements, appraisal with 1007 rent schedule, operating statements, insurance binder, credit report, ID, entity docs for LLCs, and property tax info.

Q: How does borrower financial strength influence DSCR loan terms?

A: Borrower financial strength influences DSCR loan terms by shifting rates and pricing: higher credit and larger reserves lower rates and increase lender flexibility; higher leverage or weak reserves raises pricing and tightens conditions.

Q: How do lenders adjust NOI and predict debt service in underwriting?

A: Lenders adjust NOI by subtracting verified operating expenses and vacancy allowances from rent. They stress‑test with higher vacancy and management fees and use qualifying payment assumptions for debt service calculations.

Q: What interest rates, terms, and structures are common for DSCR loans?

A: DSCR loan interest rates typically range 5–9%. Loan structures include 30‑year fixed, ARMs (5/6, 7/6, 10/6), interest‑only periods of 5–10 years, and stepped prepayment penalties.

Q: How do DSCR loans differ from conventional investment mortgages?

A: DSCR loans differ from conventional mortgages by underwriting to property cash flow instead of personal income and DTI; they often allow LLC ownership but generally require higher rates and larger down payments.

Q: What practical steps improve DSCR to qualify for a loan?

A: To improve DSCR, increase NOI by raising rents or cutting expenses, refinance to lower payments, use interest‑only periods, and tighten documentation to better show actual rent and income.

Q: What is the DSCR loan application workflow and common approval pitfalls?

A: The DSCR loan application workflow runs prequalify, submit docs, appraisal + 1007, underwriting, conditions, then closing. Common pitfalls are insufficient reserves, unverifiable rents, poor DSCR, and property condition problems.