Think a DSCR of 1.0 will get you a loan? Think again.

Most lenders want a DSCR between 1.15 and 1.25, with 1.20 the practical cutoff.

Sectors like retail or hospitality, and weaker submarkets, often push minimums toward 1.40 or higher.

This post lays out the core minimums lenders use, how underwriters stress-test DSCR, and simple, realistic steps to improve your coverage so you know what lenders expect and what to do next.

Core Minimum DSCR Standards Lenders Use for Approval

Most conventional commercial lenders want a DSCR somewhere between 1.15 and 1.25, with 1.20 acting as the practical cutoff. Your property’s net operating income needs to be at least 20 percent higher than your annual debt service. Investment property lenders usually set minimums between 1.20 and 1.40, depending on what you’re buying, where it’s located, and how the market looks. Stable assets in strong markets tend to sit at the lower end. Higher risk properties or weaker submarkets push that minimum closer to 1.40.

Small business loans target around 1.20. SBA programs often start at 1.15. Fannie Mae and Freddie Mac multifamily lenders typically want at least 1.25 for stabilized market-rate properties. High-risk sectors like retail or hospitality get tougher scrutiny. Lenders in those spaces often demand 1.50 or higher to account for revenue swings and the elevated default risk during downturns.

Any DSCR below 1.0 means your property doesn’t generate enough income to cover the loan payments. Some lenders will make exceptions if you bring compensating factors like a bigger down payment, strong credit, deep cash reserves, or a track record managing similar properties. But those exceptions don’t happen often, and they usually come with higher rates or tighter terms.

| Loan Type | Typical Minimum DSCR | Notes |

|---|---|---|

| Conventional Commercial | 1.15–1.25 | Common threshold is 1.20; lower minimums require strong compensating factors |

| Multifamily Agency (Fannie/Freddie) | 1.25 | Higher for special-needs or small-unit properties; adjusts with cap rates |

| SBA 7(a) / 504 | 1.15 | Varies by guarantor and industry risk; personal guarantees often required |

| High-Risk Sectors (Retail/Hospitality) | 1.50+ | Lenders demand larger cushion due to revenue volatility and cyclical downturns |

Explaining DSCR and How It Works in Underwriting

DSCR stands for Debt Service Coverage Ratio. Lenders use it to figure out if your property or business generates enough income to cover the loan payments with a cushion left over. The formula is simple: take your net operating income and divide it by your total annual debt service. Net operating income is your revenue minus operating expenses, before you subtract debt payments, depreciation, or income taxes. Debt service is the total principal and interest you owe each year.

A DSCR of 1.0 is break-even. Your income exactly matches your debt payments. If you’re at 1.25, you’re generating 25 percent more income than you need to cover the loan. Higher interest rates increase your debt service and lower your DSCR. Longer amortization periods reduce your annual payment and improve your DSCR. That’s why borrowers often stretch from a 20-year to a 30-year term to hit minimum thresholds.

Here’s how to calculate it:

- Start with gross income from the property or business for the year.

- Subtract all operating expenses (property taxes, insurance, utilities, maintenance, management fees) to get your net operating income.

- Add up 12 months of principal and interest payments to get total annual debt service.

- Divide NOI by debt service.

Example: If your property generates $100,000 in NOI and your annual debt service is $80,000, your DSCR is 1.25. You’re producing 25 percent more income than required to cover the loan payment.

DSCR Requirements by Specific Lender Categories and Underwriting Nuances

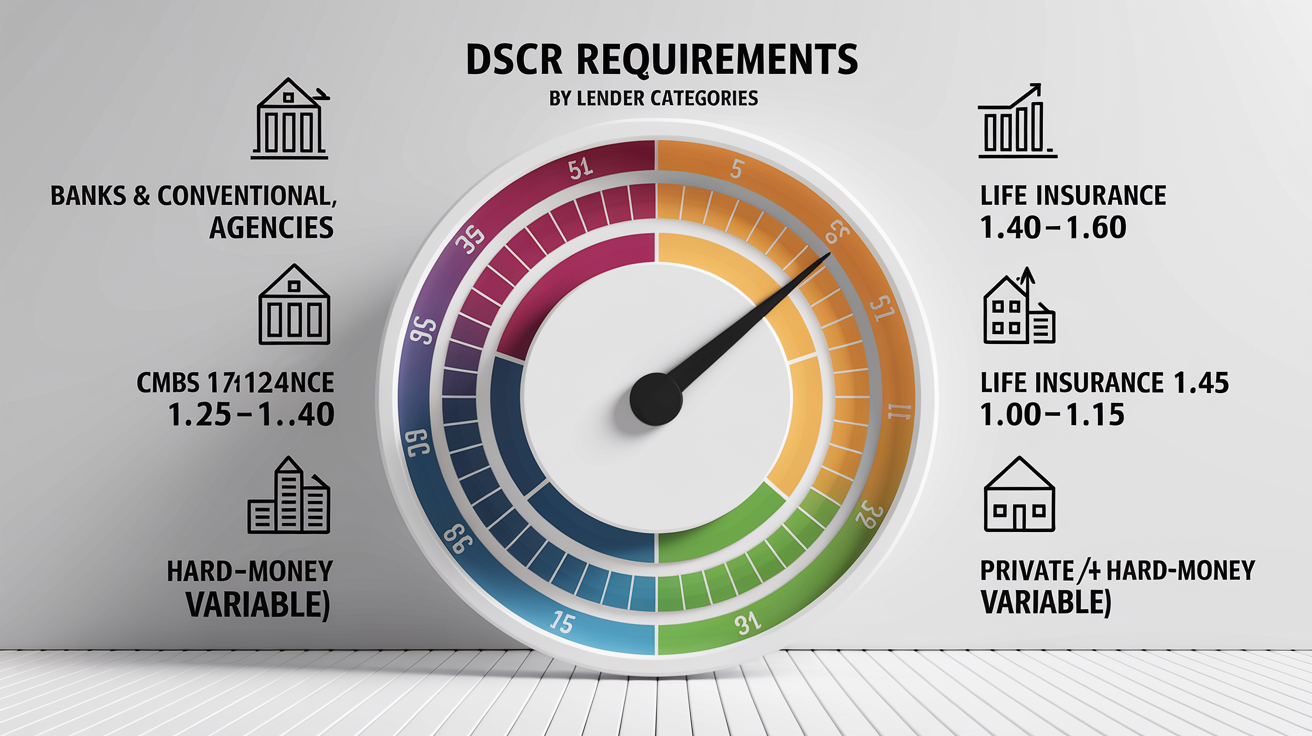

Fannie Mae and Freddie Mac multifamily lenders usually want a minimum DSCR of 1.25 for stabilized market-rate properties. Special-needs housing, affordable housing with program overlays, or very small unit counts can push that minimum higher. SBA 7(a) and 504 loans typically set the floor around 1.15, though individual lenders and industry risk can shift that number. Personal guarantees and strong borrower financials help SBA borrowers qualify at the lower end.

CMBS lenders commonly require minimums between 1.25 and 1.40. They also run stress tests during underwriting, recalculating DSCR at higher interest rates or lower occupancy to see if the loan can survive adverse conditions. Your actual DSCR might need to be 1.30 or higher to pass their stress-test floor of 1.25. Life insurance companies take a conservative approach with long-term fixed-rate loans and often require minimums between 1.40 and 1.60. They offer some of the lowest rates and longest terms available in exchange.

Bridge lenders and value-add lenders accept much lower minimums, often between 1.00 and 1.15. They’re focused on your repositioning plan and exit strategy, not your current cash flow. If you’re buying a property to renovate and stabilize, a bridge lender cares more about your after-repair value and take-out financing than what you’re making today. Private lenders and hard-money lenders sometimes accept DSCR below 1.0 or ignore it completely, relying instead on loan-to-value and exit strategy. Their underwriting is asset-based and short-term, so they’ll tolerate negative cash flow if the equity cushion and repayment plan make sense.

Here’s a breakdown by lender type:

Banks and conventional commercial lenders: Minimum DSCR typically 1.15 to 1.25. 1.20 is the practical floor for approval without heavy compensating factors.

Agencies (Fannie/Freddie multifamily): Minimum DSCR usually 1.25. Higher for properties with elevated risk or smaller unit counts.

CMBS/conduit lenders: Minimum DSCR 1.25 to 1.40, with mandatory stress testing that can effectively raise the threshold another 5 to 10 basis points.

Life insurance companies: Minimum DSCR often 1.40 to 1.60. Conservative underwriting in exchange for long-term fixed rates and high leverage on the best deals.

Bridge and value-add lenders: Minimum DSCR 1.00 to 1.15. They’ll accept lower current coverage if the stabilization plan and exit financing are credible.

Private/hard-money lenders: DSCR minimums vary widely. Some require none at all and focus entirely on LTV, exit strategy, and borrower experience.

Factors That Affect the Minimum DSCR Lenders Will Require

Higher loan-to-value ratios almost always push lenders to demand higher DSCR minimums. If you’re borrowing 80 to 85 percent of the property’s value instead of 70 to 75 percent, the lender’s risk goes up and they’ll often bump the minimum DSCR from 1.25 to 1.30 or higher. Rising interest rates increase your annual debt service, which lowers your DSCR for any given NOI. When rates climb, lenders know your coverage cushion shrinks, so they sometimes raise their minimums to maintain the same risk tolerance they had at lower rates.

Market conditions and economic uncertainty also shift lender behavior. During periods of volatility or anticipated recession, lenders tighten underwriting standards and raise minimum DSCR requirements across the board. Conservative lenders run interest-rate stress tests by recalculating your DSCR at 50 to 100 basis points higher than the actual note rate. They also model vacancy adjustments, assuming your occupancy drops 5 to 20 percent below current levels. If your property still clears their minimum DSCR under those stress scenarios, you pass underwriting. If not, you’ll need to bring more equity or improve the property’s income.

Lender-specific policy overlays mean two banks can look at the same property and require different minimums. Life insurance companies and pension-fund lenders expect higher DSCR because they’re deploying long-term capital and want maximum stability. Community banks and credit unions might accept slightly lower DSCR if you have a strong deposit relationship or local market knowledge. Property type also matters. A single-tenant net-lease property with a creditworthy tenant might qualify at 1.20, while a multi-tenant retail center in a secondary market could require 1.35 or higher.

How to Meet or Improve Minimum DSCR Requirements

The fastest way to raise your DSCR is to increase net operating income. That means raising rents to market rate, improving occupancy through better marketing or property upgrades, cutting operating expenses by shopping for cheaper insurance or renegotiating vendor contracts, or adding ancillary income like parking fees, laundry, or storage. If you need an extra $15,000 in NOI to hit a DSCR of 1.25, figure out whether that’s easier to achieve through a 5 percent rent increase across your units or by trimming $1,250 per month from your expense line.

Lowering your debt service is the other option. Refinancing to a lower interest rate or extending your amortization from 20 years to 30 years can reduce your annual payment by 15 to 25 percent, depending on the rate environment. Paying down high-interest debt early or reducing your loan size by bringing more equity to the table both lower debt service and improve DSCR. Some borrowers use interest-only periods on bridge loans to minimize debt service during the repositioning phase, then refinance into permanent financing once the property stabilizes and DSCR improves.

Here are five ways to meet or improve minimum DSCR requirements:

- Increase NOI: Raise rents to market, improve occupancy through better tenant screening or unit upgrades, reduce operating costs by shopping insurance and renegotiating contracts, or add new revenue sources like fees or premium services.

- Cut operating expenses: Audit your property-tax assessment and file appeals if overassessed, switch to more efficient utilities or negotiate bulk rates, reduce management fees by self-managing or renegotiating your contract.

- Restructure the loan: Refinance to a lower interest rate, extend amortization to 25 or 30 years to lower annual payments, or reduce the loan amount by increasing your down payment or equity contribution.

- Build cash reserves: Accumulate 6 to 12 months of operating reserves. Lenders sometimes accept lower DSCR if you demonstrate a strong liquidity cushion to cover shortfalls.

- Add guarantors or co-borrowers: Bring in a partner with strong credit and income, or offer a personal guarantee to offset borderline DSCR. Some lenders will adjust their minimum threshold if the overall borrower profile strengthens.

How Lenders Verify DSCR and Required Documentation

Lenders require detailed financial documentation to confirm that your stated DSCR is accurate and sustainable. For rental properties, they’ll ask for 12 to 24 months of rent rolls showing tenant names, lease terms, monthly rent, and any delinquencies. They’ll also request two years of operating statements, profit-and-loss reports, or tax returns that reconcile your gross income and operating expenses to arrive at net operating income. If you’re using pro forma NOI based on planned rent increases or repositioning work, you’ll need appraisal market-rent analyses and detailed budgets to support those projections.

Leases are critical for verifying income stability. Lenders review lease agreements to confirm rent amounts, escalation clauses, tenant creditworthiness, and remaining lease terms. They cross-check your rent roll against executed leases and bank deposits to catch any overstatements. Appraisers provide independent market-rent opinions, and if the appraiser’s market rent comes in lower than your lease, the lender will use the lower number in the DSCR calculation. Occupancy reports and trailing payment histories help lenders assess collection risk and the likelihood that your current NOI will hold up over the loan term.

Core documents lenders request for DSCR verification:

Rent rolls: Monthly snapshots showing tenant names, unit numbers, lease start/end dates, current rent, and any delinquencies or concessions.

Operating statements: Two years of profit-and-loss statements or tax returns (Schedule E for smaller properties, full financials for commercial) that show gross income, itemized operating expenses, and net operating income.

Appraisal market-rent analysis: Independent third-party opinion of achievable rent based on comparable properties. Lenders use this to validate or adjust your stated income.

DSCR Calculation Examples for Meeting Minimum Requirements

Example A shows a loan with annual debt service of $80,000 and a lender minimum DSCR of 1.25. To meet that threshold, your property must generate net operating income of at least $100,000, because $100,000 divided by $80,000 equals 1.25. If your current NOI is $95,000, you’re $5,000 short and need to raise rents, cut expenses, or bring more equity to lower the loan amount and debt service.

Example B shows a property with NOI of $150,000 and annual debt service of $120,000. Dividing $150,000 by $120,000 gives you a DSCR of 1.25, which meets most conventional and agency minimums. That property produces $30,000 more in annual income than required to cover the debt, giving the lender a comfortable cushion and you some breathing room for vacancies or unexpected repairs.

Example C models a $1,000,000 loan at 5.0 percent interest amortized over 30 years. The approximate annual payment is $64,400. If the lender requires a minimum DSCR of 1.20, you’ll need NOI of at least $77,280 to qualify, calculated as $64,400 multiplied by 1.20. If your property generates $85,000 in NOI, your DSCR is 1.32, which not only meets the minimum but also qualifies you for better pricing and terms.

| Scenario | NOI | Debt Service | Resulting DSCR | Meets Minimum? |

|---|---|---|---|---|

| Example A | $100,000 | $80,000 | 1.25 | Yes (meets 1.25 minimum) |

| Example B | $150,000 | $120,000 | 1.25 | Yes (meets 1.25 minimum) |

| Example C | $77,280 | $64,400 | 1.20 | Yes (meets 1.20 minimum) |

Common DSCR Mistakes That Lead to Falling Below Minimum Requirements

Overestimating rental income is the most frequent error. Borrowers use aspirational rents or peak-season rates instead of conservative market-rent comps. When the appraiser delivers a lower market-rent opinion, your DSCR calculation drops and you no longer meet the lender’s minimum. Ignoring seasonality is another trap, especially for properties in tourist markets or college towns where occupancy swings 20 to 40 percent between peak and off-peak months. Lenders want to see stabilized, annualized NOI, not cherry-picked high months.

Excluding balloon payments or variable interest from your debt-service calculation understates your true annual obligation. If your loan includes a balloon payment due in year five, or if your interest rate can adjust after an initial fixed period, lenders will model those payments into their DSCR analysis. Misclassifying capital expenditures as one-time costs instead of recurring reserve items also distorts NOI. Rising property taxes, insurance premiums, or HOA fees eat into your NOI over time. Underestimating those line items at closing means your DSCR deteriorates faster than you planned. Vacancy sensitivity is often underestimated. A drop from 95 percent to 85 percent occupancy can push a borderline DSCR below 1.0 and trigger a loan covenant default.

Final Words

in the action we covered lender minimum ranges, how DSCR is calculated, lender-specific rules, factors that change the ratio, and steps to raise it.

Quick take: conventional lenders roughly 1.15–1.25; multifamily agencies ≥1.25; SBA about 1.15; high-risk sectors often 1.50+. We included worked examples and common mistakes to avoid.

Run the quick DSCR screen, collect rent rolls and operating statements, and stress-test your NOI. That will show whether you hit the minimum DSCR ratio lenders require. Do the prep and you’ll be ready to move forward with confidence.

FAQ

Q: What minimum DSCR do lenders typically require by loan type?

A: The minimum DSCR lenders typically require by loan type is: conventional commercial 1.15–1.25; multifamily agencies ≥1.25; residential investment 1.20–1.40; SBA ≈1.15; high‑risk sectors often ≥1.50.

Q: How is DSCR calculated?

A: DSCR is calculated as NOI divided by debt service, where NOI is income minus operating expenses and debt service is annual principal plus interest; for example $100,000 NOI ÷ $80,000 debt service = 1.25.

Q: How do lender types and underwriting nuances change DSCR requirements?

A: Lender types and underwriting nuance change DSCR requirements: banks and CMBS usually expect 1.25–1.40 and stress test; life companies 1.40–1.60; bridge and private lenders may accept 1.00–1.15 or lower with conditions.

Q: What factors cause lenders to raise the minimum DSCR?

A: Factors that cause lenders to raise the minimum DSCR include higher loan‑to‑value, interest‑rate sensitivity, weak local market conditions, property type risk (like retail or hospitality), and tighter lender policy or stress testing.

Q: How can I improve my DSCR before applying for a loan?

A: To improve DSCR before applying, raise NOI by increasing rents or occupancy, cut operating costs, refinance to lower payments or extend amortization, build cash reserves, or add a guarantor.

Q: What documents do lenders require to verify DSCR?

A: Lenders require documents to verify DSCR such as 12–24 months of rent rolls, two years of operating statements, current leases, occupancy reports, appraiser market‑rent analysis, and pro forma stabilization projections.

Q: What are common DSCR mistakes that cause denial or weak underwriting?

A: Common DSCR mistakes that cause denial include overestimating rents, ignoring seasonality, excluding balloon or variable payments, misclassifying expenses, and underestimating taxes, insurance, or capex needs.

Q: What does a DSCR below 1.0 mean and can a lender still approve the loan?

A: A DSCR below 1.0 means projected NOI doesn’t cover debt service; a lender might still approve with offsets like lower LTV, extra equity, reserves, guarantees, or a clear exit plan, but approval is harder.