What if your rent could pay most of your mortgage?

House hacking does exactly that.

You live in a place and rent parts of it so tenants help cover the bill.

For beginners this means practical options you can start with fast, like renting spare bedrooms, buying a duplex and living in one unit, adding an ADU, or renting parking and storage.

This post walks you through how each strategy works, the upfront costs, how to finance it with low down payment loans, and simple checks to make sure the numbers actually save you money.

Core Beginner House Hacking Methods Explained Clearly

House hacking works by turning your primary residence into a rental income source. You live in the property, invite tenants to help cover costs. Simple goal: reduce or eliminate your monthly housing expense while building equity in a place you already call home.

The most accessible strategies fall into a few buckets. Rent spare bedrooms to long-term roommates or rotate short-term guests through Airbnb. Buy a duplex, triplex, or fourplex, live in one unit, rent the others. Convert underused space (basement, garage, big backyard) into a rentable apartment or ADU. Some beginners even rent parking spaces or storage to generate smaller but consistent income.

Each method balances privacy, upfront cost, and management effort differently. Renting a bedroom costs the least to start but means sharing common areas. Multifamily properties offer more separation but need higher down payments and more tenant coordination. Short-term rentals can produce higher nightly rates but demand active hosting and compliance with local STR rules.

What follows: how to pick the right property type, secure financing with low down payments, calculate monthly savings, execute each strategy, manage tenants, stay legal, avoid common mistakes, and scale over time.

Single-family spare room rental – Rent one or more bedrooms to housemates in your owner-occupied home.

Small multifamily live-in – Purchase a 2 to 4 unit building, occupy one unit, rent the rest.

Accessory dwelling unit (ADU) – Build or convert a basement, garage, or backyard cottage into a separate rental.

Short-term rental (Airbnb/Vrbo) – Rent part of your home nightly or weekly to traveling guests.

Parking or storage rental – Lease your driveway, garage, or shed to neighbors or online marketplace users.

Live-in flip – Buy a fixer-upper, renovate while living there, rent rooms during rehab, then sell or refinance after two years.

Choosing the Right House Hacking Property Type

Beginners should match property type to their financial capacity, lifestyle preferences, and long-term goals. A single-family home with extra bedrooms needs the smallest down payment and simplest financing but offers limited rental income compared to a fourplex. A duplex or triplex increases rental revenue and provides physical separation from tenants, yet it costs more upfront and may need commercial insurance or stricter zoning approvals.

Think through privacy tolerance first. Sharing walls or common spaces with tenants works for some people and feels intrusive to others.

Financing ease matters. Residential lenders underwrite 2 to 4 unit properties using the same loan programs available for single-family homes, so you can access FHA, VA, or conventional financing with low down payments. Properties with five or more units require commercial loans that demand higher credit scores, larger down payments, and shorter amortization schedules. Zoning and local occupancy laws also filter your choices: some municipalities cap the number of unrelated adults per dwelling, prohibit ADUs, or ban short-term rentals outright. Check municipal codes before you tour properties.

Long-term scalability influences which property type to start with. A fourplex generates more monthly rent than a duplex, accelerating equity growth and cash reserves for your next purchase. When you move out after the required one-year occupancy period, a fourplex converts into a full rental that can fund another house hack. Single-family homes with basement apartments offer a middle path (easier resale than multifamily properties but lower rental upside). Run pro forma projections on at least three property types in your target market before committing.

Privacy needs – Rate your tolerance for shared walls, entrances, kitchens, or yards on a 1 to 10 scale, then eliminate property types below your threshold.

Financing eligibility – Confirm which loan products and down payment ranges you qualify for, then search for properties that fit those limits.

Zoning and occupancy rules – Look up local codes on maximum occupants, ADU permits, and short-term rental allowances before narrowing your search.

Exit strategy – Model the property as both a live-in hack and a future full rental or resale to make sure it works in both scenarios.

Financing Essentials for Beginner House Hackers

Owner-occupied financing gives house hackers a decisive advantage over traditional investors. Because you commit to living in the property for at least one year, lenders offer lower down payments, better interest rates, and more flexible underwriting than they provide for pure investment properties. Most beginner-friendly programs accept projected rental income as part of your debt-to-income ratio, making it easier to qualify even if the mortgage stretches your current budget.

| Loan Type | Minimum Credit Score | Down Payment | Key Features |

|---|---|---|---|

| FHA | ~580+ | 3.5% | 1-year occupancy; mortgage insurance required; up to 4 units |

| Conventional | ~620+ | 3–20% | PMI under 20% down; flexible terms; no occupancy cap on portfolio |

| VA | No minimum | 0% | One-time funding fee; eligible veterans only; up to 4 units |

| HomeReady / Home Possible | ~620+ | 3% | Counts projected rent; reduced mortgage insurance; income limits apply |

FHA Loans

FHA loans require a minimum credit score around 580 and accept down payments as low as 3.5 percent. You can purchase a property with up to four units and still qualify for this residential financing. On a $350,000 duplex, 3.5 percent down equals $12,250, a much smaller barrier than the $70,000 conventional 20 percent deposit. FHA loans do require mortgage insurance for the life of the loan unless you refinance or pay it down below 78 percent loan-to-value, and you must live in the property for at least one year as your primary residence. If you move out before the year ends, the loan can be called due or reclassified.

Conventional Loans

Conventional loans typically require a credit score of 620 or higher and offer down payment options between 3 and 20 percent. Putting down less than 20 percent triggers private mortgage insurance (PMI), which adds to your monthly payment but drops off automatically once you reach 20 percent equity through principal paydown or appreciation. Conventional financing doesn’t cap how many properties you can own over time, making it the preferred path for investors planning to grow beyond one or two house hacks. Rates are competitive, and underwriting standards are well-defined.

VA Loans

VA loans offer 0 percent down payment financing to eligible veterans and active-duty service members. Instead of monthly mortgage insurance, the VA charges a one-time funding fee that can be rolled into the loan. Interest rates are often lower than FHA or conventional products, and the VA allows purchases of up to four-unit properties. You still must occupy the property for at least one year. If you qualify, VA financing removes the largest barrier to entry (saving a down payment) and maximizes your starting position.

HomeReady & Home Possible

HomeReady (Fannie Mae) and Home Possible (Freddie Mac) programs accept down payments as low as 3 percent and allow lenders to count projected rental income when calculating your debt-to-income ratio. These programs target low to moderate income borrowers and impose income limits based on area median income. Mortgage insurance rates are often reduced compared to standard conventional loans. Home Possible caps you at two properties with a combined four units, limiting long-term portfolio growth, while HomeReady offers slightly more flexibility. Both programs can make a marginal deal qualify when your current income alone falls short.

Calculating Cash Flow and Monthly Savings for House Hackers

Before you make an offer, run a simple rent-versus-mortgage calculation to confirm the property will actually reduce your housing costs. Start with the total monthly mortgage payment: principal, interest, property taxes, homeowners insurance, and any mortgage insurance. Add estimated utilities, maintenance reserves (budget 1 percent of the home value annually), and a vacancy buffer of 5 to 8 percent of gross rent. Subtract the total monthly rent you expect to collect from tenants. The difference is your net monthly housing cost. If that number’s lower than your current rent or drops to zero, the house hack works.

A worked example makes this concrete. Buy a five-bedroom house for $625,000 with 20 percent down. Your monthly mortgage payment, taxes, and insurance total $3,500. Utilities and maintenance reserves add another $200, bringing total monthly expenses to $3,700. Rent four bedrooms at $800 each for $3,200 monthly income. Subtract $3,200 from $3,700, and you pay $500 out of pocket (an 87 percent reduction from typical market rent of $2,500 for a comparable one-bedroom apartment). If you rent one room short-term for $1,000 instead of $800 long-term, your net cost drops to $300.

Always pressure-test your assumptions. Model a scenario where one bedroom sits vacant for two months and another tenant pays late. Factor in a surprise $2,000 HVAC repair or property tax increase. If those events push your monthly cost above your current rent, the margin’s too thin. Cash flow positive means rental income exceeds all monthly expenses including reserves; most beginner house hacks aim for break-even or modest positive cash flow in year one, then improve margins by raising rents or refinancing to lower the mortgage payment.

Step 1: Add principal, interest, taxes, insurance, and mortgage insurance to find total monthly debt service.

Step 2: Estimate utilities, internet, trash, and any HOA fees you won’t charge back to tenants.

Step 3: Budget 1 percent of the purchase price annually for maintenance and repairs, divide by 12 for monthly reserve.

Step 4: Multiply expected monthly rent by 0.92 (8 percent vacancy buffer) to find conservative rental income.

Step 5: Subtract total expenses (steps 1 to 3) from conservative income (step 4) to find net monthly housing cost.

Executing House Hacking with Spare Rooms, ADUs, and Converted Spaces

Renting spare bedrooms in a single-family home requires the least upfront capital and fastest setup. Prepare the room with basic furniture, a lock on the door, and a clean shared bathroom. Set fair market rent by checking Craigslist, Facebook Marketplace, or Airbnb comparables for similar rooms in your neighborhood. Write a simple month-to-month lease or room rental agreement that covers rent amount, due date, utility split, house rules, and notice period. Screen tenants by verifying income, checking references, and running a basic background check even for informal roommates. Living with someone who doesn’t pay or causes conflict is far more stressful than managing a tenant in a separate unit.

Building or converting an ADU increases upfront cost but delivers higher rent and better privacy. A garage conversion typically costs $30,000 to $80,000 depending on local permit fees, utility hookups, insulation, and finish quality. A ground-up backyard cottage runs $100,000 to $200,000 in most markets. Check zoning codes first. Many cities now allow ADUs by right, but setback rules, maximum square footage, owner-occupancy requirements, and parking mandates vary widely. Once permitted and built, an ADU rents for 60 to 80 percent of a comparable one-bedroom apartment, often $1,200 to $2,000 monthly, and adds significant resale value to the main property.

Short-term rentals through Airbnb or Vrbo can generate higher nightly rates than long-term leases ($80 to $150 per night in mid-tier markets versus $800 to $1,200 per month for the same space). The trade is active management: you handle bookings, guest communication, cleaning between stays, and restocking basics like toilet paper and coffee. Many municipalities now regulate or ban short-term rentals, so verify local rules before listing. If allowed, start with one bedroom or a basement suite, keep a simple check-in process, and use dynamic pricing tools to adjust rates by season and local events.

Occupancy guidelines like the “2+1 rule” (two people per bedroom plus one extra) give a rough legal maximum, but local ordinances override that formula. Some cities cap unrelated adults at three or four per household regardless of square footage. Confirm your local limits before signing multiple roommates or converting spaces.

Spare room rental: Furnish minimally, set rent at 70 to 85 percent of studio apartment rates, use written lease, screen income and references.

Basement apartment conversion: Budget $20,000 to $50,000 for egress window, separate entrance, kitchenette, bathroom upgrade, and permits.

Detached ADU build: Expect $100,000 to $200,000 all-in; verify setback and height rules; plan 6 to 12 month permit and construction timeline.

Short-term rental setup: Check municipal STR license requirements, furnish to hotel standard, photograph professionally, price 20 to 30 percent below nearby hotels.

Beginner Tenant Management and Operational Basics

Set up a repeatable tenant screening process before you list the first room or unit. Require every applicant to complete a written application with employment history, current income, references, and permission to run a background check. Verify income at three times the monthly rent (if rent is $1,000, the tenant should earn at least $3,000 gross per month). Call previous landlords to confirm on-time payment and no property damage. Run a credit and criminal background check through a service like TransUnion SmartMove or RentPrep. Document everything. Discrimination laws apply even to informal roommate selection, so use objective criteria and apply them consistently to every applicant.

Use a written lease agreement for every tenant, including housemates in a shared living arrangement. The lease should specify rent amount, due date, late fees, security deposit, maintenance responsibilities, house rules (guests, noise, parking), notice period for move-out, and lease term (month-to-month or fixed). Even a simple one-page room rental agreement signed by both parties protects you if disputes arise. Collect the first month’s rent and security deposit (typically one month’s rent) before handing over keys. Deposit security funds in a separate account if your state requires it, and document the property condition with photos at move-in and move-out.

Use property management or accounting software to automate rent collection and track income and expenses from day one. Platforms like Avail, TurboTenant, or Stessa let tenants pay rent online, generate automatic receipts, track maintenance requests, and produce year-end reports for tax filing. Most landlord expenses (mortgage interest, property taxes, insurance, repairs, utilities, and depreciation) are tax-deductible on the rental portion of your property. Keeping accurate records simplifies filing Schedule E and maximizes deductions. Set aside time each month to reconcile accounts and maintain a separate emergency fund equal to three to six months of mortgage payments and expenses.

Application: Require written application with income, employment, rental history, and authorization to run background check.

Income verification: Request recent pay stubs or bank statements showing gross monthly income at least 3× the rent.

Reference check: Call previous landlords to confirm payment history and property condition at move-out.

Background screening: Run credit report and criminal background check through a compliant third-party service.

Lease execution: Use written lease specifying rent, deposit, rules, and notice period; collect first month’s rent and security deposit before move-in.

Legal & Zoning Rules for Safe Beginner House Hacking

Local zoning and occupancy laws determine whether your house hacking plan is legal. Some municipalities limit the number of unrelated adults who can live together in a single-family home (often three or four) regardless of square footage. Multi-family zoning typically allows by-right rentals, but single-family zones may prohibit separate leases or require owner-occupancy for ADUs. Short-term rentals face the most restrictions: many cities now require STR licenses, cap the number of nights per year, or ban them entirely in residential neighborhoods. Look up your property’s zoning designation and read the municipal code section on rentals, accessory structures, and occupancy limits before you buy or list tenants.

Fair housing laws apply to tenant selection even when you share living space. You can’t discriminate based on race, color, religion, national origin, sex, familial status, or disability under federal law, and many states add protections for source of income, sexual orientation, or gender identity. Use objective screening criteria (income level, credit score, rental history) and apply them to every applicant. Document your reasons for accepting or rejecting candidates. Informal “roommate preference” posts that specify gender, age, or lifestyle can still trigger fair housing complaints, so focus on property features and lease terms instead of personal characteristics.

Insurance requirements change when you rent part of your home. Standard homeowners policies typically exclude coverage for rental activity or limit liability for tenant injuries. Notify your insurance carrier that you’re renting rooms or units and ask whether you need a landlord or dwelling fire policy. Landlord insurance costs more but covers rental income loss, tenant-caused damage, and higher liability limits. If you use a separate structure like an ADU, confirm that it’s covered under your policy or add an endorsement. Umbrella liability policies (often $1 million for $200 to $400 annually) provide extra protection against lawsuits and are worth considering once you have tenants.

Common Beginner Mistakes in House Hacking and How to Avoid Them

New house hackers often underestimate vacancy and model cash flow assuming 100 percent occupancy year-round. Real rental properties experience turnover, and even well-screened tenants move out with 30 days’ notice. Budget a 5 to 8 percent vacancy rate into your projections. If you expect $3,000 monthly rent, plan for $2,760 on average. Surprise vacancies hurt less when you have an emergency fund covering three to six months of mortgage payments. If your margin depends on every bedroom staying full every month, the first vacancy will create financial stress and force poor decisions like accepting an unqualified tenant.

Weak tenant screening is the second most common error. Skipping background checks or accepting tenants who earn less than three times the rent leads to late payments, evictions, and property damage. Living next door to a problem tenant is far more stressful than managing a distant rental property. Use the same objective criteria for every applicant, verify income and references, and trust your instinct if something feels off during the showing. The cost of a $40 background check is trivial compared to months of unpaid rent and eviction legal fees.

Misunderstanding loan occupancy requirements can trigger loan default or fraud allegations. FHA, VA, and conventional owner-occupied loans require you to live in the property as your primary residence for at least one year from closing. Moving out after six months to start another house hack violates the loan terms. Lenders can call the loan due, report fraud, or deny future financing. Plan to stay the full year, then convert the property to a full rental or refinance into an investment loan before buying your next primary residence. Ignoring this rule isn’t worth the risk.

Vacancy buffer: Always model 5 to 8 percent vacancy even if current tenants seem stable; turnover happens, and you need cash reserves to cover gaps.

Tenant screening shortcuts: Never skip income verification, reference checks, or background reports to fill a room faster; bad tenants cost far more than one month’s vacancy.

Occupancy requirement ignorance: Stay in the property for the full 1-year owner-occupancy period required by your loan; moving early can trigger loan default.

Insurance gaps: Notify your carrier about rental activity and upgrade to landlord or dwelling fire coverage before the first tenant moves in.

Underestimating rehab or maintenance costs: Budget 1 percent of home value annually for repairs and set aside extra cash for emergency fixes like HVAC or roof leaks.

Legal and zoning research failures: Confirm local occupancy limits, ADU rules, and STR regulations before signing a purchase contract or listing tenants.

Scaling a Portfolio After Your First House Hack

After the required one-year owner-occupancy period, you have two main options: stay in the property and continue house hacking, or move out and convert all units to rentals. Moving out turns your first property into a pure investment. If the rental income exceeds the mortgage and expenses, you now have positive cash flow and a growing equity position. That rental income can help you qualify for a second owner-occupied loan on your next house hack, accelerating portfolio growth. Lenders typically allow you to count 75 percent of documented rental income toward your debt-to-income ratio once you have a signed lease and a history of on-time payments.

Refinancing after 12 to 24 months lets you lower your monthly payment, remove mortgage insurance if you have 20 percent equity, or pull cash out for your next down payment. Property appreciation and loan paydown often push your loan-to-value ratio below 80 percent within two years, especially in appreciating markets. A cash-out refinance extracts equity while keeping the property as a rental. If your fourplex appraised at $285,000 after you bought it for $220,000, you can refinance up to 75 percent LTV on an investment property (around $213,000), pay off the original loan, and pocket the difference minus closing costs. That cash funds the down payment on your second house hack.

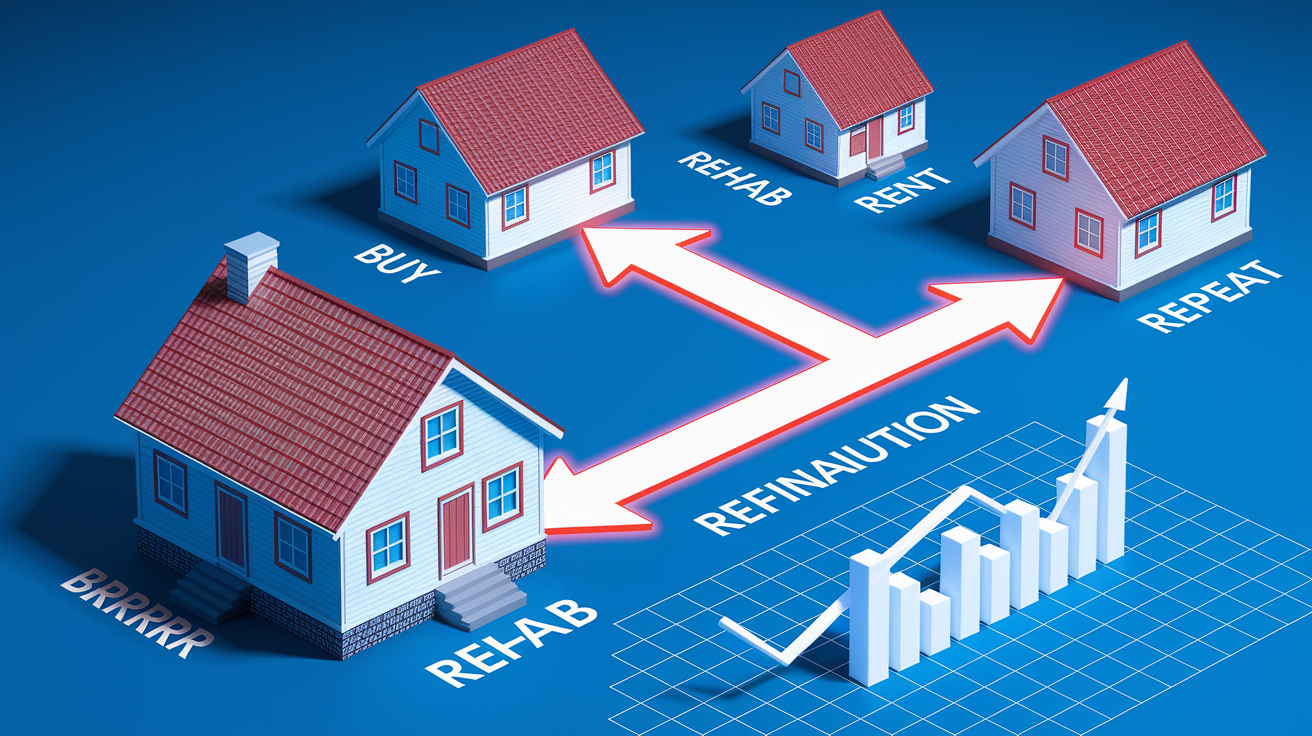

The BRRRR method (Buy, Rehabilitate, Rent, Refinance, Repeat) formalizes this scaling approach. Buy a distressed property with owner-occupied financing, renovate it while living there, rent out the extra units or rooms, refinance once the property appraises higher after improvements, and use the extracted equity to repeat the process. This method works best when you have renovation skills or reliable contractors, enough cash reserves to fund the rehab, and a market where forced appreciation through improvements is feasible. After two or three successful cycles, you can own multiple cash-flowing properties with minimal capital left in each deal.

Long-term portfolio building combines house hacking with traditional buy-and-hold investing. Each time you move, the previous property becomes a rental. After 10 to 15 years and three to five properties, rental income can exceed your living expenses, creating financial independence. The key is to maintain low debt levels, keep emergency reserves for each property, and avoid over-borrowing during market peaks. House hacking provides the foundation (low down payment entry, owner-occupied financing rates, and hands-on landlord education), but scaling requires discipline, patient capital deployment, and systematic tenant management across multiple properties.

| Strategy | Timeline | Key Action | Outcome |

|---|---|---|---|

| Move-out and rent all units | After year 1 | Convert entire property to rental, move to next owner-occupied purchase | Positive cash flow, portfolio growth, rental income counts toward next loan |

| Refinance to lower payment | 12–24 months | Refinance to remove PMI or lower rate once equity exceeds 20% | Improved monthly cash flow, reduced expenses, stronger debt service coverage |

| Cash-out refinance | 24+ months | Pull equity out at 75% LTV, use cash for next down payment | Capital for second property, maintain rental income, use appreciation gains |

| BRRRR cycle | 12–18 months per cycle | Buy distressed, renovate, rent, refinance to 75% of new value, repeat | Rapid portfolio growth, minimal capital per property, forced appreciation |

Final Words

Rent spare rooms, live in one unit of a duplex, add an ADU, or try short-term rentals. These are the practical entry paths you can use right away. Pick a property type that fits your privacy needs, financing options, and long-term goals.

We covered owner-occupied loan choices (FHA, conventional, VA), simple cash-flow checks, tenant screening, permits, and the common mistakes to avoid.

Do a quick screen, hold reserves, and run the numbers. These house hacking strategies for beginners can cut housing costs and build equity. Start small and learn as you go.

FAQ

Q: What is the 3 3 3 rule in real estate?

A: The 3 3 3 rule in real estate is a quick screening heuristic: keep about three months of cash reserves, assume roughly 3% vacancy, and budget about 3% annual maintenance; it varies by market.

Q: What is the 70% rule in flipping houses?

A: The 70% rule in flipping houses says buy at no more than 70% of the after-repair value (ARV) minus rehab costs, preserving margin for profit, holding costs, and surprises.

Q: What devalues a house the most?

A: The thing that devalues a house the most is major deferred maintenance or structural problems, like foundation, roof, or water damage, because they cut the buyer pool and need costly repairs; location also matters long term.

Q: Can my mom sell me her house for $1?

A: Selling a house to a child for $1 is legally possible but usually treated as a gift, which can trigger gift-tax reporting, mortgage due-on-sale issues, reassessment for property taxes, and lender scrutiny; get tax and legal advice.