What if your tenants paid most of your mortgage?

House hacking means you live in a property and rent out parts of it so other people help cover the mortgage, taxes, insurance, and repairs.

Do it right and you can cut or erase your monthly housing cost, build equity in the same property, and learn landlord skills without buying a second home.

This post shows how it works, who it’s best for, and the simple checks to see if a house hack will actually help you.

What Is House Hacking? (Simple Definition for Beginners)

House hacking means you live in a property and rent out part of it so tenants cover some (or all) of your housing costs. Instead of paying the entire mortgage yourself, your renters chip in on the monthly payment, taxes, insurance, and upkeep.

Most people use this to make homeownership cheaper. It turns your personal residence into a small rental operation without needing a separate investment property or a pile of extra cash. You’re there, you manage it, and you collect rent that makes ownership affordable right away.

How House Hacking Works

You buy (or already own) a home with extra space. Could be spare bedrooms, a basement, a converted garage, or separate units. You live in one part and rent the rest to tenants. Their rent goes straight toward your mortgage, taxes, and other ownership costs.

Here’s a simple example: your mortgage runs $2,000 a month. You rent two bedrooms at $700 each. That’s $1,400 coming in, which drops your actual housing cost to $600. Rent enough space at the right price and you might live free. Or even pocket a little cash while building equity in something you own.

The setup’s straightforward, but details matter. You’ll track income, follow landlord laws, keep both your space and the rental areas in shape, and deal with vacancies when someone leaves. The payoff? You’re not carrying the full load alone, and you’re learning real estate while living inside the deal.

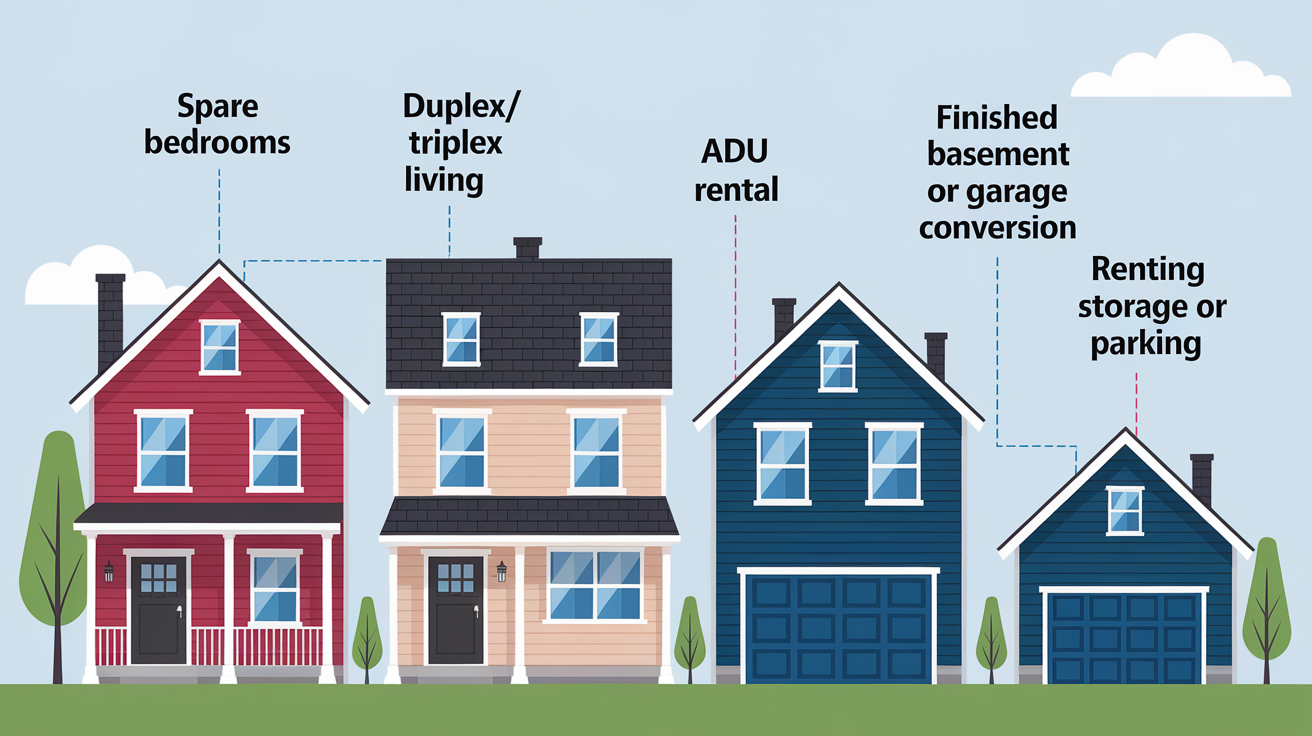

Common House Hacking Methods

What you choose depends on your budget, the property you can buy (or already have), and how much you’re okay with sharing your space.

Renting spare bedrooms gets you started with a single-family home that has extra rooms. Rent them to long-term tenants or short-term guests. Works if you don’t mind sharing the kitchen and living room.

Duplex, triplex, or fourplex living means buying a small multifamily building, living in one unit, and renting the others. You get separate spaces and usually better cash flow than renting individual rooms.

Accessory Dwelling Unit (ADU) rental involves adding (or renting out) a detached cottage, in-law suite, or backyard unit. ADUs give you and your tenant real privacy, but they can need zoning approval and cost money upfront to build.

Finished basement or garage conversion turns unused square footage into a rentable apartment with its own entrance, kitchen, and bathroom. Adds property value and creates a clearly defined tenant area.

Renting storage, parking, or other assets means leasing your driveway, garage, pool, or yard to neighbors or local businesses. Less work than managing tenants, but usually brings in less money.

Picking the right method comes down to how much privacy you need, how much money you have for upgrades, and what your local zoning and HOA rules let you do. If you’re cautious or just testing this out, start small with one bedroom. If you want better separation and stronger cash flow, look for a duplex or triplex where you live in one unit and rent the others.

Step-by-Step Guide to Starting House Hacking

House hacking isn’t hard, but it needs planning before you buy or before you start renting space you already own.

-

Check your finances and set a budget. Figure out how much mortgage you can handle if tenants don’t pay for a few months. Calculate your target monthly payment (principal, interest, taxes, insurance) and estimate how much rent you need to bring that number down.

-

Research local zoning, HOA rules, and landlord-tenant laws. Not every city or neighborhood allows ADUs, basement apartments, or short-term rentals. Check before you buy or renovate. Skipping this can cost you thousands in fines or shut down your rental income entirely.

-

Choose your property type and strategy. Decide if you want a single-family home with extra rooms, a small multifamily property, or something with conversion potential. Match it to your budget and how much tenant contact you can handle.

-

Secure financing. Compare FHA loans (3.5 percent down), VA loans (zero down for eligible veterans), and conventional options. Some programs let you count future rental income when qualifying, which helps you afford more property.

-

Buy the property or prepare your current home. If you’re buying, target properties already set up for rentals or easy to convert without major expense. If you’re using your current place, budget for repairs, permits, and safety upgrades like separate entrances or fire doors.

-

Make necessary improvements and prepare rental spaces. Fix plumbing, electrical, paint, and flooring before you advertise. Tenants pay more for clean, working spaces, and you dodge repair calls during the first month.

-

Find and screen tenants. Run credit and background checks, call prior landlords, and set clear lease terms. Use a written lease covering rent, utilities, house rules, and move-out expectations.

Success early on looks like this: your first tenant moves in without drama, rent shows up on time, and your net housing cost drops noticeably. That’s your signal you’ve set things up right and can think about scaling or doing this again later.

Financial Benefits of House Hacking

The biggest win is obvious: someone else helps pay your mortgage. Instead of spending $2,500 a month on rent or a loan payment, you might spend $800 after tenant rent covers the rest. That extra cash can go toward student loans, retirement savings, or your next property down payment.

House hacking also speeds up wealth building. You’re living in an asset that appreciates while tenants pay down the loan. Every month your equity grows without you writing the full check. Hold the property long enough and you can move out, keep it as a rental, and repeat the process with a new house hack.

Lower monthly housing expenses. Rent collected reduces or wipes out your cost.

Faster savings and investment capital. Money you don’t spend on housing can fund other goals.

Equity buildup funded by tenants. Your renters pay down the mortgage principal while you live there.

Potential tax deductions. You may deduct a portion of mortgage interest, property taxes, repairs, and depreciation for the rented space. Work with a tax professional to get this right.

Entry into real estate investing without a second property. You learn landlord skills, deal evaluation, and tenant management while living in the deal, not from a distance.

Realistic House Hacking Examples

These scenarios show how different property types and strategies affect monthly cash flow and net housing cost.

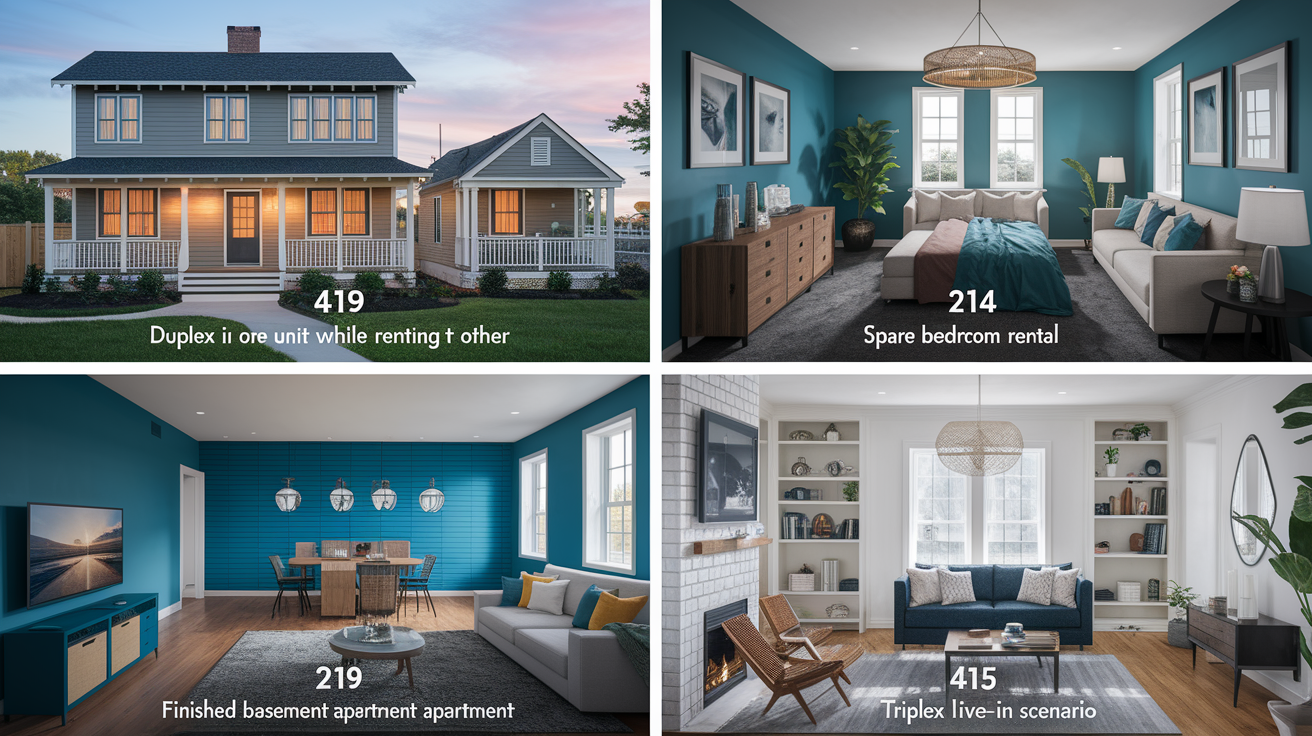

Duplex house hack. You buy a duplex for $350,000 with an FHA loan (3.5 percent down). Your monthly mortgage runs $2,300. You live in one unit and rent the other for $1,400. Your net cost is $900 per month, plus you’re building equity in a $350,000 asset.

Spare bedroom rental. You own a three-bedroom house with an $1,800 mortgage. You rent two bedrooms to working professionals at $650 each. That’s $1,300 in monthly rent, dropping your housing cost to $500. You share the kitchen and living room but keep the owner’s suite private.

Finished basement apartment. Your mortgage is $2,000. You spend $15,000 converting the basement into a one-bedroom unit with a separate entrance. You rent it for $1,100 per month. After one year you’ve recovered part of the renovation cost, and your net housing expense is $900 ongoing.

Triplex live-in scenario. You buy a triplex for $375,000 with a $2,388 monthly payment at 6.8 percent interest. You rent two units at $1,400 each. That’s $2,800 in rent, giving you a $412 monthly surplus after the mortgage. You live for free and pocket extra cash.

What you can learn from these: the more units or rentable space you control, the better your cash flow potential. Single-room rentals are easier to start but usually won’t cover the whole mortgage. Multifamily properties take more capital upfront but can flip your housing cost to positive income if the numbers work.

Requirements and Qualifications for House Hacking

Most low-down-payment loans (FHA, VA, Freddie Mac Home Possible) require you to live in the property as your primary residence. That usually means occupying one unit for at least 12 months. Move out earlier and the lender can call the loan or reclassify it as an investment property with different terms.

Zoning and local ordinances control what you’re allowed to rent. Some cities restrict ADUs, limit the number of unrelated tenants in a single-family home, or ban short-term rentals entirely. HOAs can add their own rules on top of city law. Check before you buy or start renovations, because a zoning violation can shut down your rental income and cost you in fines or forced reversals.

Owner-occupancy requirement. You must live in one unit if using FHA, VA, or similar programs.

Sufficient credit and income to qualify. Lenders review your debt-to-income ratio. Some programs let you count future rental income toward qualification.

Down payment. Ranges from zero percent (VA) to 3.5 percent (FHA) to higher percentages for conventional or investment loans.

Property condition and safety standards. FHA and VA loans require the property to meet minimum livability standards before closing.

Legal permission to rent. Verify zoning, HOA, and city rental licensing requirements before advertising for tenants.

Pros and Cons of House Hacking

Pros:

Lowers monthly housing costs dramatically, sometimes to zero or negative. Builds real estate experience and landlord skills without owning a separate investment property. Lets you use low-down-payment, owner-occupied financing instead of pricier investment loans. Potential tax deductions on mortgage interest, property taxes, repairs, and depreciation for the rented portion. Speeds up equity growth as tenants help pay down your mortgage.

Cons:

Living with tenants reduces privacy and can create friction over shared spaces or house rules. You take on landlord responsibilities like repairs, tenant screening, lease enforcement, and potential evictions. Rental income isn’t guaranteed. Vacancies mean you cover the full mortgage yourself. Zoning, HOA, or city rules may limit what you can rent or how many tenants you can have. Maintenance, insurance, and taxes still apply, and unexpected repairs can wipe out cash flow quickly.

If you value autonomy and quiet, sharing walls or common areas might feel like too much compromise. If you’re focused on lowering costs and learning investing, the tradeoffs usually make sense for a year or two while you build savings and experience.

Costs and Expenses to Expect

Even with rental income, you’re still responsible for the property’s full operating cost. Knowing what to budget keeps you from getting surprised when the water heater dies or a tenant moves out mid-lease.

Your regular monthly obligations include the mortgage (principal and interest), property taxes, homeowners insurance, and possibly HOA fees. If you pay utilities for tenant spaces, add electric, water, gas, trash, and internet. Some house hackers split utilities. Others include them in rent and charge accordingly.

Repairs and maintenance are ongoing. Budget 1 to 4 percent of the property’s purchase price per year for routine upkeep like paint, appliance fixes, HVAC service, and landscaping. Or set aside 5 to 8 percent of gross rental income each month as an operating reserve.

Mortgage, taxes, and insurance (PITI). Your baseline monthly cost.

Utilities. Electricity, water, gas, trash, internet if you cover them.

Routine maintenance and repairs. HVAC tune-ups, plumbing fixes, appliance replacements.

Vacancy loss. Plan for one or two months per year without a tenant paying rent.

Property management fees. If you hire help, expect 8 to 12 percent of monthly rent.

Renovation or conversion costs. Upfront spending to create rentable space (basement finish, ADU build, garage conversion).

Licensing, permits, and legal compliance. Some cities require rental licenses or inspections.

If your monthly mortgage is $2,000 and you collect $1,500 in rent, don’t assume you’re pocketing $500 every month. After maintenance reserves, vacancy allowance, and occasional larger repairs, your real monthly benefit might be closer to $300. Run conservative numbers and you won’t get stuck when reality shows up.

Tips and Best Practices for Beginners

Start by picking a property and strategy that matches your risk tolerance and available time. If you’ve never been a landlord, renting one bedroom in your current home is a lower-stakes way to learn before you buy a fourplex.

Screen tenants carefully. Run credit and background checks, call previous landlords, and trust your gut if something feels off during the interview.

Set clear house rules from day one. Who pays utilities, when is rent due, what are quiet hours, how do guests and parking work? Put it in writing.

Budget conservatively for rent and vacancy. Assume you’ll have at least one month per year without rental income, and don’t count on maximum market rent until you’ve proven you can get it.

Keep good records for taxes. Track all rental income, repair receipts, and operating expenses. You’ll need them at tax time and if you ever get audited.

Maintain boundaries and communication. Be responsive when tenants report problems, but don’t let the landlord role take over your personal life. Use texts, emails, and scheduled check-ins instead of constant interruptions.

Understand local landlord-tenant law. Know the rules for security deposits, lease termination, eviction procedures, and required disclosures. Ignorance isn’t a defense if you violate tenant rights.

The goal is to make house hacking feel manageable, not like a second full-time job. If you set systems early (screening process, lease template, repair vendor list, rent collection method), you’ll spend less time troubleshooting and more time benefiting from the rent checks.

Common House Hacking Mistakes to Avoid

New house hackers often underestimate costs and overestimate rental income. They assume full occupancy at top-of-market rent, then panic when a tenant leaves or haggles over price.

Skipping due diligence on zoning and HOA rules. Buying a property only to discover you can’t legally rent it out is an expensive mistake. Always verify before you close.

Failing to screen tenants properly. Renting to the first person who applies because you need the income fast can lead to late payments, property damage, or eviction headaches.

Underbudgeting for repairs and vacancy. If you assume zero downtime and no maintenance costs, the first $2,000 plumbing bill will wipe out months of profit.

Ignoring tax and legal obligations. Rental income is taxable, and landlord-tenant laws vary by state and city. Not reporting income or violating Fair Housing rules can cost you in fines or lawsuits.

Choosing the wrong financing. Using a conventional investment loan with 20 percent down when you qualify for FHA at 3.5 percent wastes capital you could deploy elsewhere.

Mixing personal boundaries with landlord duties. Being too friendly or too hands-off creates confusion. Treat it like a business relationship with professional boundaries, even if your tenant lives ten feet away.

Most of these mistakes come from rushing or wishful thinking. Take time to run real numbers, check local rules, and set up proper systems before you collect the first rent check. The deal should work on paper with conservative assumptions. If it only works when everything goes perfectly, it’s not a solid house hack.

Final Words

Rent spare rooms, live in one unit, and let rental income cut your housing bill.

This post showed what house hacking is, how it works, common methods, step-by-step startup actions, the money math, rules to check, and common mistakes.

Next steps: run a quick number screen, verify zoning and loan rules, and line up honest tenant screening and reserves.

If you still ask what is house hacking and how it works, start small and pressure-test the numbers. It can trim your housing cost and move you toward real equity.

FAQ

Q: Can someone sell your house without you knowing?

A: Someone can sell your house without you knowing only in rare cases, such as fraudulent title transfers, abused power of attorney, or an heir selling after probate; normally the owner must sign closing paperwork.

Q: What devalues a house the most?

A: What devalues a house the most are poor location, major structural or environmental problems, and prolonged deferred maintenance, because they cut buyer demand and lower comparable sale prices.

Q: How do you know if your house is being cased?

A: You know a house is being cased if strangers repeatedly observe, photograph, or note entry points and schedules, loiter nearby, ask odd questions about occupancy, or leave unusual markings or signs.

Q: How long do you have to live in a place to house hack?

A: How long you have to live in a place to house hack depends on loan and local rules; commonly lenders expect 6–12 months, while FHA needs occupancy within 60 days and usually one year.